The EU is deindustrialising; Czech industry is helping to reverse the trend

21 Dec. 2015 | CzechInvest | The Czech Republic had a very positive outcome in the European Commission’s new EU Structural Change Report 2015, which evaluates the European Union from the perspective of manufacturing structures and specialisation over the past 15 years.

A fundamental long-term trend detailed by the report consists in the transition of the European Union’s economy from manufacturing to services, i.e. deindustrialisation. However, the reduction of production capacity impacts exports and the innovation potential of the economy, which to a significant degree deserve credit for long-term growth and a higher standard of living. The growth of the services sector is also resulting in the exclusion of certain types of products manufactured in the EU from international markets. Reversal of this trend and restoration of a sustainable level of production in the manufacturing industry has therefore been one of the main priorities of the EU in recent years. The European Commission wants to achieve a strong industrial base in future and thus also a larger share of the manufacturing industry in the structure of the member countries’ economies. Despite the declining share of the manufacturing industry in the overall structure of the EU economy, the production sector is not deteriorating, as it may seem at first glance. Credit for this is due mainly to countries like the Czech Republic, where the manufacturing industry has historically been strong.

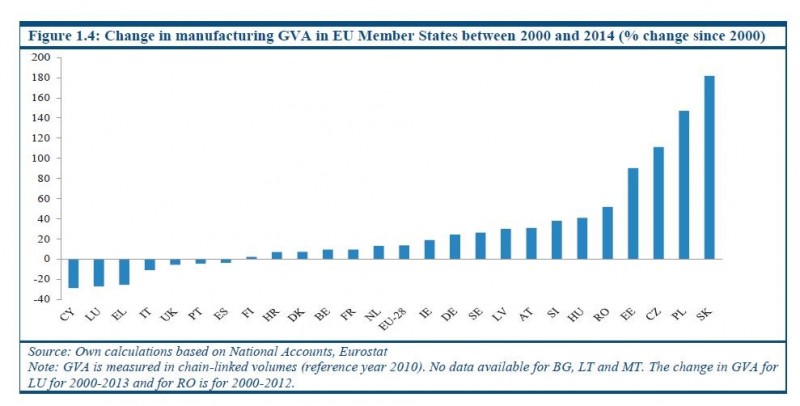

According to the report, which covers the period 2000-2014, the Czech Republic ranks among the countries with the highest growth of gross value added in the manufacturing industry. The countries, GVA growth rate is specifically 111%. Only Poland and Slovakia recorded higher percentage growth in the same period, with 147% and 182%, respectively (see graph 1). The Czech Republic achieved significant improvement also in terms of employment in the high-tech, medium/high-tech and medium/low-tech sectors, where more jobs were created. Furthermore, in the past 15 years the Czech Republic has managed to significantly increase labour productivity, unlike Poland, for example.

Graf 1 (source: EU Structural Change 2015)

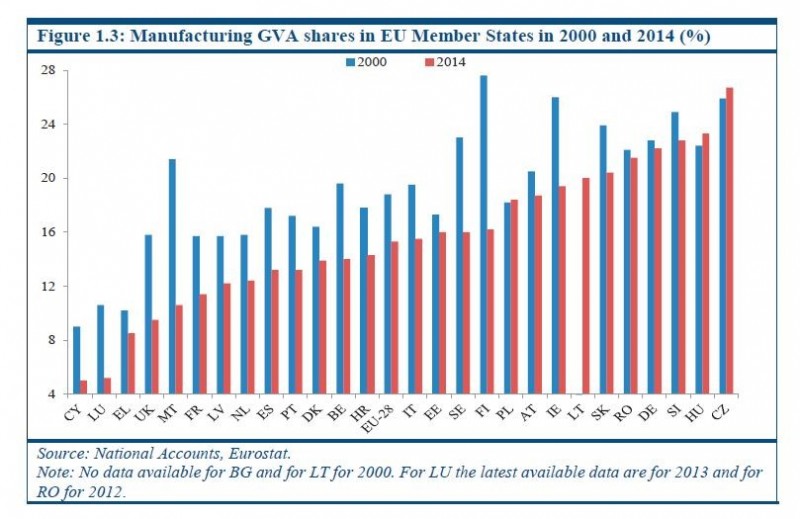

Graph 2 shows the share of value added in the manufacturing industry in individual EU member countries in 2000 and 2014. The Czech Republic is among the best of the EU’s 28 members, as it displays nearly identical values from both years and the highest value in the EU in 2014. It is thus apparent that most of the EU countries recorded a decline in the level of value added in the manufacturing industry; only the Czech Republic, Hungary and Poland recorded growth.

Graph 2 (source: EU Structural Change 2015)

The Czech Republic also increased production in the medium/low-tech, medium/high-tech and high-tech sectors. In the high-tech sector, 200% growth was recorded in the period from 2000 to 2012. This striking difference was the result of growth in the production of computer, electronic and optical products, which was not so widespread here in 2000.

Among other things, the report also breaks down investments in physical production capital, which are an important engine of economic growth and should ideally represent 20% to 25% of a given country’s GDP. The average amount of gross fixed capital in the EU comprised 22.1% in 2000, but only 19.3% in 2014. Most EU member countries thus recorded a substantial decline of investment following 2007-2008, when investment volumes peaked. For example, the volume of investments in Greece fell by 65% in comparison with the period 2007-2008. Conversely, in the Czech Republic in 2014 gross fixed capital comprised 25% of GDP, i.e. the ideal value. Among the other EU member countries, only Estonia did as well as the Czech Republic.

The full report is available for download here.